Car Loans After Bankruptcy:Your Fresh Start Begins Here

Bankruptcy was your financial reset, not the end of car ownership. Our dealer network has helped thousands of post-bankruptcy customers get reliable transportation.

Car Loan After Bankruptcy Timeline

Most dealers consider a car loan after bankruptcy as soon as you have a discharge date (Chapter 7) or trustee approval (Chapter 13). Expect lenders to weigh income stability and the vehicle budget more than the past filing.

Income, Down Payment, & Budget

A realistic down payment ($500-$1,500) plus provable income beats credit history. That's how many customers secure a chapter 7 car loan soon after discharge.

Chapter 13 Auto Financing

For chapter 13 auto financing, lenders want trustee approval and proof the payment fits your plan. We guide you to dealers who handle this every week.

Bankruptcy should be a financial reset, not a permanent roadblock. The right dealer will size the vehicle and payment to your current budget so you can rebuild credit with on-time payments.

Need next steps? Apply in 60 seconds to see local dealer options, then bring your discharge papers (or trustee approval), proof of income, and proof of residence. We'll connect you with a lender who works with post-bankruptcy buyers daily.

Why Bankruptcy Doesn't Disqualify You

Chapter 7 Bankruptcy

Chapter 7 eliminates most unsecured debts, giving you a clean slate. After discharge (typically 3-6 months), you're eligible to apply for new credit.

- Can apply immediately after discharge

- No existing debt obligations to consider

- Focus is on current income ability

Chapter 13 Bankruptcy

Chapter 13 sets up a repayment plan over 3-5 years. You may be able to get a car loan during repayment with trustee approval.

- Shows commitment to repaying debts

- May qualify with trustee approval

- Demonstrates payment discipline

Post-Bankruptcy 90-Day Rebuild Plan

Follow this simple path to secure financing and use the loan to rebuild your credit after bankruptcy.

Week 1: Prepare Your File

Gather discharge papers, proof of income (pay stubs or bank statements), proof of residence, and a realistic budget. This is what underwriters want to see for any car loan after bankruptcy.

Weeks 2-3: Apply & Get Matched

Complete the 60-second form and take the dealer call. If you're in Chapter 13, request trustee approval so you can move forward with chapter 13 auto financing.

Weeks 4-12: Make On-Time Payments

Choose a modest vehicle, make every payment on time, and consider refinancing in 12-18 months. Many buyers with a chapter 7 car loan refinance once their score improves.

How Post-Bankruptcy Auto Financing Works

Our process is designed specifically for credit-challenged buyers. Here's what to expect.

Pre-Qualify Online (60 Seconds)

Fill out our quick form with your basic info. We don't pull your credit. We just need enough to match you with the right dealer. Include your bankruptcy status and discharge date if applicable.

Get Matched with a Specialist Dealer

We connect you with a local dealership that specifically handles post-bankruptcy financing. Their finance managers have relationships with lenders who specialize in your situation.

Consultation Call

A financing specialist calls to verify your income, discuss your situation, and explain your options. They'll give you a realistic payment range (typically $150-$850/month depending on the vehicle).

Visit the Dealership & Drive

Bring your ID, proof of income, and bankruptcy discharge papers. Because financing is largely pre-arranged, you're there to pick your vehicle and finalize terms. Many customers drive home the same day.

What Our Dealers Look For

Bankruptcy is just one factor. Here's what actually matters for qualification.

Current Income

Your current ability to pay matters most. W-2 employment, 1099 gig work, Social Security, disability. All count. Multiple income sources are combined.

Job Stability

Lenders like to see steady employment. Even if you recently started a new job, history in your field or consistent gig income helps.

Down Payment

Having $500-$1,500 shows commitment and reduces lender risk. Trade-ins with equity count toward down payment. Some programs offer lower requirements.

Car Loan After Chapter 13 Discharge

Chapter 13 discharge is different from Chapter 7. Here's what lenders look for and how to position yourself for approval.

A car loan after Chapter 13 dischargeis very achievable. You've just completed 3-5 years of court-supervised repayment, which actually works in your favor. Lenders see Chapter 13 completion as proof that you can stick to a payment plan.

Chapter 13 vs. Chapter 7: What Lenders Care About

After Chapter 13 Discharge

- Completed full repayment plan

- Demonstrated 3-5 years of payment discipline

- Some lenders offer better rates than Ch. 7

- Stays on credit report 7 years from filing

After Chapter 7 Discharge

- Clean slate with debts eliminated

- Can apply immediately after discharge

- No existing debt obligations

- Stays on credit report 10 years from filing

If you're currently still in Chapter 13 repayment and need a vehicle, you can often get financing with trustee approval. The court understands that reliable transportation is essential for maintaining employment and completing your repayment plan. Your attorney can help you file a motion to incur new debt.

What to Bring to the Dealership After Bankruptcy

Getting organized before your dealership visit speeds up the process. Whether you had a Chapter 7 or Chapter 13 filing, have these documents ready:

Required Documents

- • Bankruptcy discharge papers

- • Recent pay stubs (last 30 days)

- • Government-issued photo ID

- • Proof of residence (utility bill or lease)

- • Social Security card or ITIN

Helpful Extras

- • Bank statements (last 2-3 months)

- • Trustee approval letter (Chapter 13)

- • List of references (personal and work)

- • Down payment or trade-in vehicle info

- • Proof of insurance (or ability to obtain)

How a Post-Bankruptcy Auto Loan Rebuilds Your Credit

A car loan after bankruptcy isn't just transportation — it's one of the fastest tools to rebuild your credit score.

Auto loans are installment credit, which credit scoring models weight heavily. Each on-time payment reports to all three major bureaus (Equifax, Experian, TransUnion) and demonstrates that you can manage debt responsibly after bankruptcy.

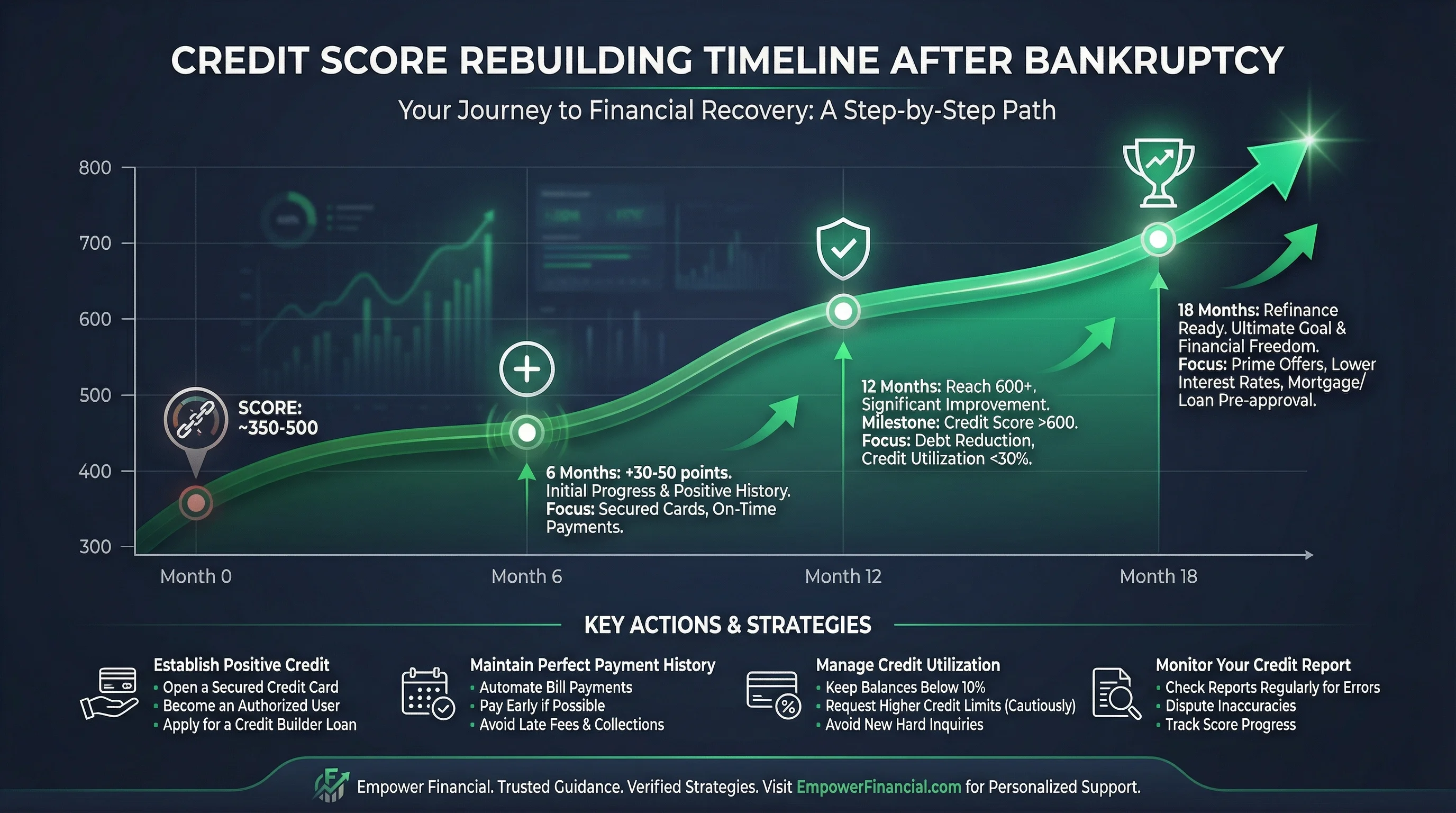

Typical Credit Score Trajectory After Bankruptcy Auto Loan

6 months

Initial score improvement of 30-50 points with consistent payments

12 months

Many borrowers reach 600+ and qualify for better rates

18 months

Refinance opportunity — lower your rate and payment

Pro tip: Set up automatic payments to ensure you never miss a due date. Even one late payment on a post-bankruptcy loan can set back your credit recovery significantly. If your budget allows, paying $25-50 extra toward principal each month reduces total interest and builds equity faster.

Ready to start rebuilding? Our dealer network specializes in bad credit auto loans and understands that your bankruptcy was a fresh start, not the end of the road. You can also estimate your monthly payment to budget before applying.

Frequently Asked Questions

How soon after bankruptcy can I get a car loan?

Many of our dealer partners can work with you immediately after bankruptcy filing or discharge. Chapter 7 filers often qualify right after discharge. Chapter 13 filers may qualify while still in repayment with trustee approval. Each situation is unique, but bankruptcy alone doesn't disqualify you.

Is Chapter 7 or Chapter 13 bankruptcy better for getting a car loan?

Neither is inherently 'better' - our dealers work with both. Chapter 7 provides a clean slate after discharge (typically 3-6 months). Chapter 13 shows you're actively repaying debts, which some lenders view favorably. The key factors are your current income and ability to make payments.

Will I need a large down payment after bankruptcy?

Down payment requirements vary, but expect $500-$1,500 for most situations. A larger down payment improves your terms and shows commitment. Some customers with strong income have qualified with minimal down payment. Your dealer will discuss options based on your specific situation.

What interest rate should I expect after bankruptcy?

Post-bankruptcy rates typically range from 15-24% APR depending on time since discharge, current income, and down payment. While higher than prime rates, this is an opportunity to rebuild credit. Many customers refinance to lower rates after 12-18 months of on-time payments.

Can I include my spouse as a co-applicant?

Yes, absolutely. Adding a co-applicant with income can strengthen your application and potentially improve your terms. We've helped many couples where one spouse had bankruptcy on their record. Combined household income is what matters most.

What documents do I need for a post-bankruptcy car loan?

Bring your bankruptcy discharge papers, proof of income (pay stubs or bank statements), valid ID, and proof of residence. If you're in Chapter 13, you may need trustee approval documentation. Your dealer will guide you through exactly what's needed.